Debt Review Removal South Africa

Welcome to Salham & Partners

For Professional legal debt review removal assistance

You've Come to The Right Place

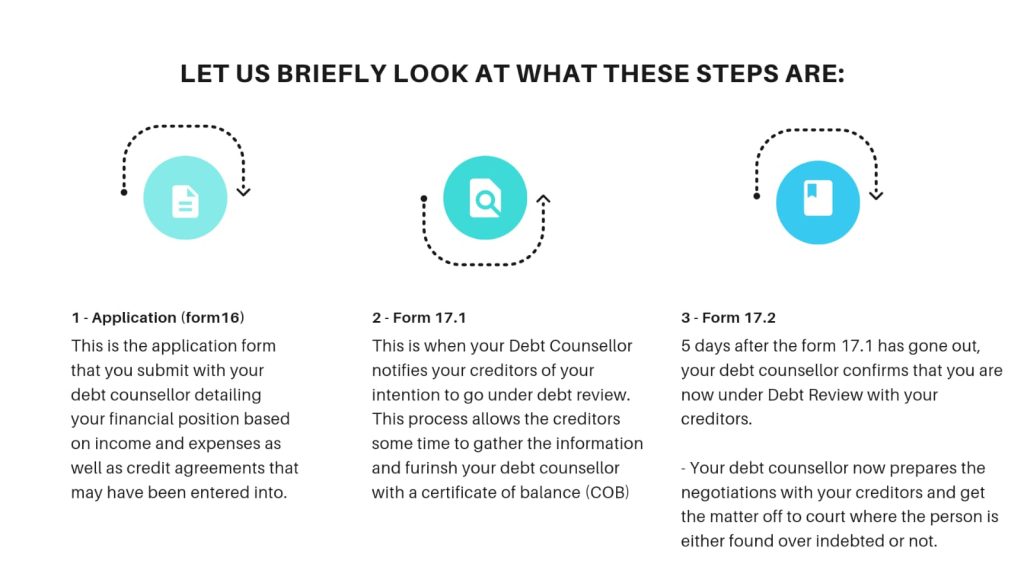

Many South Africans have heard of Debt Review under the National Credit Act. 34 of 2005 but not all are familiar with what its all about. Debt Review is a formal debt solution that is governed by the National Credit Act in passed in 2005.

This process requires commitment and has proven to provide great relief to many South Africans who have been struggling with debt. This commitment however is not always the solution for many and for some, the decision to go under debt review may have been a hasty financial decision or one that was suited at the time but is no longer needed.

In these cases, some consumers prefer to exit the commitment of debt review because it is no longer the appropriate financial solution. Circumstances change or what was said would happen doesn’t – leaving the consumer in a rather precarious financial situation.

Before embarking on an understanding of how to get out of a debt review programme, its important to understand debt review and its various stages as well as the various repercussions for exiting at these various stages. Let us help you with Debt Review Removal South Africa.

Debt Review Removal

Section 71(2)(b)(i) of the National Credit Act initially made provision for consumers to only exit debt review through issuance of a clearance certificate after they have paid all their re-arranged debts in full. The effect of this provision is that in instances where a home loan formed part of the debt review application, consumers have to remain under debt review for the duration of the home loan term even after settling re-arranged short term debts.

This provision will however change upon proclamation of the National Credit Amendment Act (NCAA) under section 71(1) as follows: (1) A Consumer whose debts have been re-arranged in terms of Part D of this Chapter must be issued with a Clearance Certificate by a Debt Counsellor within seven days after the Consumer has done one of 2 things:

1. Satisfied all the obligations

Satisfied all the obligations under every credit agreement that was subject to that debt re-

arrangement order or agreement in accordance with that order or arrangement.

2a. Demonstrated

a. financial ability to satisfy the future obligations in terms of the re-arrangement order or agreement under- (i.) an agreement which secures a credit agreement for the purchase or improvement of immovable property. (ii.)any long term agreement that may have prescribed;

2b. Demonstrated

b. that there are no arrears on the re-arrangement contemplated in subparagraph (i); and c. that all obligations under every credit agreement included in the re-arrangement order or agreement have been settled in full.

It is therefore clear and important to note that a debt counsellor alone does not have the requisite statutory powers to terminate or withdraw the debt review process. This means that the debt review flag will remain in place on the credit records whether the process has been cancelled by the Consumer or not. Speak to us about Debt Review Removal South Africa.

FREQUENTLY ASKED QUESTIONS

1. What is Debt Counselling/Debt Review?

- Debt Review otherwise known as Debt Counselling is a process where assisting all South African citizens who is over-indebted, by reducing their total monthly installments up to 50% in according to the customers household budget or expenses.

- Consumers can be placed under debt review in order to protect them from creditors and so that their assets cannot be repossessed.

- Client must be permanently employed or self- employed.

2. Will I go to court?

- Our legal team is responsible for combining all debt review court applications from documents, which are completed & signed by clients as well as their credit providers and the payments cascades that they have set up.

- The legal team asks the attorney to place the offer on a roll for a specific date. Once this has been completed, the legal team will notify the clients and their credit providers about the court date for the review case to be reviewed.

- Certain courts require the actual debt review clients to be present at the court at the time of the court order, however in the vast majority of cases, the Magistrate’s Court would rather allow the matter to be dealt with by your attorneys.

3. Once Debt Review has been removed from my name, can I take out new credit?

Our legal team is responsible for combining all debt review court applications from documents, which are completed & signed by clients as well as their credit providers and the payments cascades that they have set up.

The legal team asks the attorney to place the offer on a roll for a specific date. Once this has been completed, the legal team will notify the clients and their credit providers about the court date for the review case to be reviewed.

Certain courts require the actual debt review clients to be present at the court at the time of the court order, however in the vast majority of cases, the Magistrate’s Court would rather allow the matter to be dealt with by your attorneys.

4. How does debt removal work?

- The first step would be to assess your situation and find out where in the process you were last. Perhaps there was a court order granted or you received a 17.2 document from your debt counsellor?

- Thereafter you will be issued with a letter from your side giving the lawyer permission to begin the process of removing you from Debt Review.

5. When can a consumer be removed from Debt Review ?

1. The client will forward all relevant documents pertaining to the debt review to Salham & Partners;

2. You will be asked to consult with the attorneys office who will explain any concerns which may be unclear as well as what the process entails.

3. The attorney will make contact with the debt counsellor in order to establish the status of the debt review, and specifically whether a Court order has been granted in respect of such consumer;

4. Upon confirmation from the Debt Counsellor, the client is notified that the application may proceed and the client is informed which documents and information is required in order to draft the application.

5. These documents are: A. The client’s salary advice; B. The client’s monthly budget; C. The monthly commitments in terms of credit agreements must be specified separately from the regular monthly expenses. D. Description of why the client encountered financial difficulty that led to debt review; E. Description of the change in circumstance resulting in this application.

6. Once the relevant information is received, Salham & Partners will draft the affidavit and this will be transmitted to the client for perusal, comment and any changes that may be necessary

7. The client will then commission the affidavit and deliver the original document to Vermeulen Attorneys either personally or by courier;

8. On receipt of the affidavit, the application will be completed and a date for hearing will be obtained at Court;

9. The application will be served on the debt counsellor;

10. The attorney will represent the client at Court on the allocated date to present the application for consideration;

11. The granted order will be uplifted from Court once ready and is sent to the debt counsellor in order that they may remove the flag from the credit bureaus;

12. Once the flag is removed the debt counsellor will advise Vermeulen Attorneys and the client will be updated;

13. This concludes the application process. We are the experts you need for Debt Review Removal South Africa.